EV Charging in the U.S: Risk & Opportunity in a Shifting Market

EV Charging in the U.S: Risk & Opportunity in a Shifting Market

Electric vehicle infrastructure is fast becoming one of the most discussed investment plays in the clean mobility transition. But with shifting policies under the Trump administration and mixed market signals, where are the most strategic places to invest today?

Let’s break it down.

The Opportunity

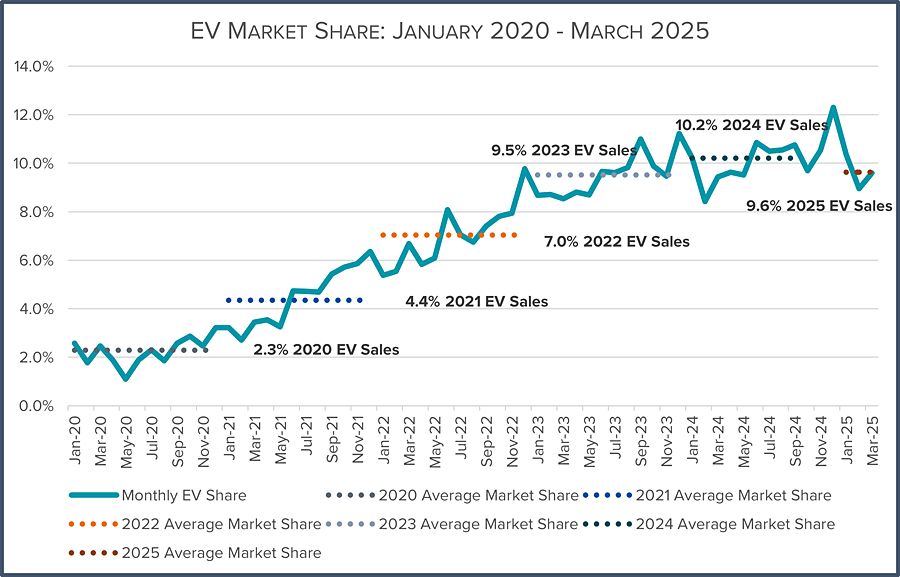

- The U.S. is the #3 EV market globally, after China and the EU, with 1.3M battery EVs sold in 2024 and a compound annual growth rate of 25.4% projected.

- Several states - including California, New York, and Maryland- have 2035 ZEV mandates in place, requiring 100% of new vehicle sales to be zero-emission by that year.

- 740,000 plug-in vehicles were sold in H1 2025, maintaining a strong ~9% monthly share.

Overall, the **installed EV base continues to grow, with more than** 4.1M EVs on U.S. roads by end of 2024, and that number is projected to reach ~5M by end of 2025.

These vehicles need regular charging, especially at retail, workplace, and travel locations where dwell times are predictable and monetizable.

The Friction

Despite strong fundamentals, short-term headwinds are real:

- EV sales dipped 6.2% in June, the third consecutive monthly decline

- Consumer openness dropped to 51% in 2025, down from 59% in 2023

With the Trump administration’s unwinding many clean energy and climate initiatives there is certainly some friction ahead.

Policy Shifts – What to Watch

Recent regulatory changes introduce both risk and clarity:

- Federal tax credit ends Sept 2025 – potentially softens short-term EV sales

- CAFE credits phased out by 2027 – affects EV automaker margins

- Home charger incentives to expire mid-2026

Federal Funding Is Still Flowing

In June 2025, a federal judge ordered the Trump administration to reinstate $5B in NEVI funds for public EV chargers.

- Unlocks projects in 14 states, including California, New York, and Washington

- Reverses a freeze that had stalled charger rollout nationwide

Let’s talk monetisation. Fundamentally these headwinds affect new EV purchases, not the charging behaviour of the millions of EVs already on the road. Infrastructure usage is tied to that installed base, which keeps growing. Undersupplied = Upside

The U.S. has only 84,000 public charging stations, with an EV-to-charger ratio of ~18:1. Compare that to: China: 10:1 EU: 13:1. Additionally, fast charger usage exceeds 25% in key cities, showing real pressure and on available infrastructure. In other words: demand is already straining supply, even before another wave of EV adoption may or may not come in.

When markets and policy are shifting, we are forced to look deeper and seek out the most strategic opportunities for monetizing EV charging.

Where to Watch: The Smart Plays

While federal policy is shifting, state-level mandates remain a backbone of EV infrastructure growth.

- California continues leading with strong policy and funding for EV networks.

- New York shows growing EV adoption, especially in dense urban regions where public charging is essential.

- Maryland shows very promising fundamentals:

- It sits within a high-traffic corridor between D.C., Baltimore, and Philadelphia

- Its legal ZEV mandate remains intact despite federal uncertainty

- And importably, its charing ratio is low, with 24:1 EVs to per station. To recap, compare that to China’s 10:1 or the US’ current 18:1 average.

We’re actively monitoring Maryland for future expansion, it has all the indicators of a high-potential untapped charging market.

Final Take

The EV market may be in a short-term reset, but the infrastructure opportunity is long-term and still growing.

States like California and New York already show strong momentum. And emerging regions like Maryland, where regulation supports growth and charger availability remains low, offer upside as policy and business environments align.

Risks are real, but so is demand. And when EV adoption rebounds, it will be the chargers already in the ground that profit first.

Related posts

Investor Update: Month 2 Performance of VOX EV Charging

Singapore's Solar Projects Earn More with RECs, How to Benefit with ReFi Hub